Earnouts and reverse earnouts are commonly used in M&A transactions to bridge valuation gaps, allocate risk, and align incentives where future performance is uncertain. While they can look similar economically, their legal and tax consequences—particularly for vendors—can differ materially depending on structure, drafting, and deal form.

The choice between an earnout and a reverse earnout is not about which is “better” in the abstract, but rather which structure best aligns certainty, tax efficiency, and risk allocation for the parties involved.

What Is an Earnout?

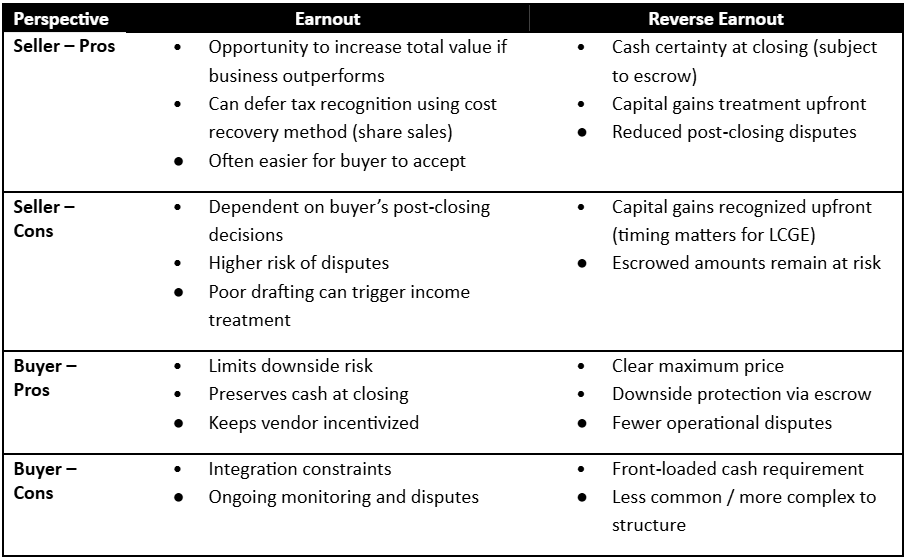

An earnout defers a portion of the purchase price and makes it contingent on post‑closing performance—typically revenue, EBITDA, or other agreed metrics over a defined period. If targets are achieved, the vendor receives additional proceeds; if not, the buyer’s total consideration is reduced.

Earnouts are most often used where:

- The vendor remains involved post‑closing

- There is uncertainty around sustainability or growth

- The buyer is seeking downside protection

What Is a Reverse Earnout?

A reverse earnout flips the mechanics. The purchase price is set at a maximum amount at closing, with a portion of that price placed at risk if post‑closing targets are not met. If performance falls short, the purchase price is reduced—typically through funds held in escrow.

Reverse earnouts are less common but can be particularly compelling in Canada where vendor tax outcomes and certainty at closing are priorities.

Seller & Buyer Perspective: Pros and Cons

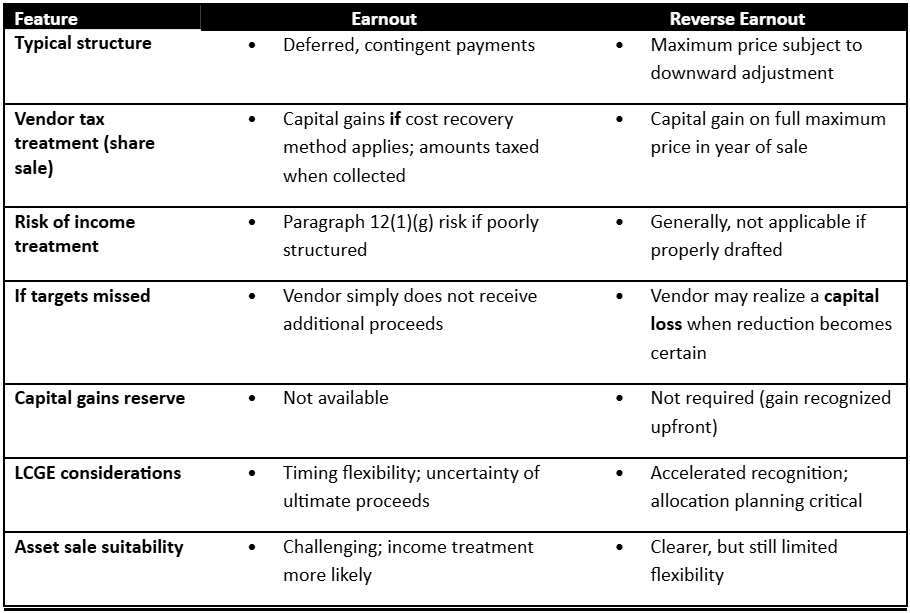

Canadian Tax Treatment: Key Differences

Practical Tax Observations (Canada)

Earnouts: Cost Recovery Is the Practical Norm in Share Sales

In arm’s‑length share transactions, earnouts are commonly structured to rely on the CRA’s administrative cost recovery method, allowing vendors to report proceeds as capital gains and recognize tax only once proceeds exceed the adjusted cost base (“ACB”) of the shares. While paragraph 12(1)(g) is often cited, it is not the typical outcome in well‑structured share deals.

That said, drafting discipline matters. Earnouts that resemble ongoing profit participation rather than purchase‑price adjustment increase risk.

Reverse Earnouts: Escrow Is Critical

For reverse earnouts to achieve their intended tax and risk allocation:

- The agreement must clearly establish a maximum purchase price

- Any reduction must be downward, not incremental

- The at‑risk amount should be held in escrow

It is tenuous for a vendor to receive at‑risk proceeds outright with an obligation to repay later. From a buyer’s perspective, escrow is strongly preferred.

LCGE and Vendor Planning

Where vendors are relying on the Lifetime Capital Gains Exemption (LCGE):

- Reverse earnouts accelerate capital gains into the year of sale

- Allocation across multiple shareholders, trusts, or family members must be planned carefully

- Earnouts may provide timing flexibility, but introduce uncertainty

These considerations should be addressed early, not after price mechanics are agreed.

Asset Sales: A Cautionary Note

Earnout planning is significantly more difficult in asset transactions:

- Cost recovery is generally unavailable

- Contingent proceeds are more likely to be treated as income

- Vendors lose much of the tax deferral flexibility available in share sales

As a result, earnouts are often less attractive to vendors in asset deals.

Final Thoughts

Earnouts and reverse earnouts are powerful—but very different—tools. In Canada, small structural differences can drive materially different tax outcomes.

- Vendors prioritizing certainty and capital gains treatment may favour a properly structured reverse earnout

- Buyers seeking downside protection may prefer a traditional earnout

- In all cases, success depends on early tax planning, disciplined drafting, and alignment between economics and legal form

Disclaimer

This article is provided for general informational purposes only and does not constitute legal or tax advice. The tax treatment of earnouts and reverse earnouts depends on the specific facts and circumstances of each transaction. Parties should obtain independent tax and legal advice before implementing any transaction structure.

Earnouts and reverse earnouts are commonly used in M&A transactions to bridge valuation gaps, allocate risk, and align incentives where future performance is uncertain. While they can look similar economically, their legal and tax consequences—particularly for vendors—can differ materially depending on structure, drafting, and deal form.

The choice between an earnout and a reverse earnout is not about which is “better” in the abstract, but rather which structure best aligns certainty, tax efficiency, and risk allocation for the parties involved.

What Is an Earnout?

An earnout defers a portion of the purchase price and makes it contingent on post‑closing performance—typically revenue, EBITDA, or other agreed metrics over a defined period. If targets are achieved, the vendor receives additional proceeds; if not, the buyer’s total consideration is reduced.

Earnouts are most often used where:

- The vendor remains involved post‑closing

- There is uncertainty around sustainability or growth

- The buyer is seeking downside protection

What Is a Reverse Earnout?

A reverse earnout flips the mechanics. The purchase price is set at a maximum amount at closing, with a portion of that price placed at risk if post‑closing targets are not met. If performance falls short, the purchase price is reduced—typically through funds held in escrow.

Reverse earnouts are less common but can be particularly compelling in Canada where vendor tax outcomes and certainty at closing are priorities.

Seller & Buyer Perspective: Pros and Cons

Canadian Tax Treatment: Key Differences

Practical Tax Observations (Canada)

Earnouts: Cost Recovery Is the Practical Norm in Share Sales

In arm’s‑length share transactions, earnouts are commonly structured to rely on the CRA’s administrative cost recovery method, allowing vendors to report proceeds as capital gains and recognize tax only once proceeds exceed the adjusted cost base (“ACB”) of the shares. While paragraph 12(1)(g) is often cited, it is not the typical outcome in well‑structured share deals.

That said, drafting discipline matters. Earnouts that resemble ongoing profit participation rather than purchase‑price adjustment increase risk.

Reverse Earnouts: Escrow Is Critical

For reverse earnouts to achieve their intended tax and risk allocation:

- The agreement must clearly establish a maximum purchase price

- Any reduction must be downward, not incremental

- The at‑risk amount should be held in escrow

It is tenuous for a vendor to receive at‑risk proceeds outright with an obligation to repay later. From a buyer’s perspective, escrow is strongly preferred.

LCGE and Vendor Planning

Where vendors are relying on the Lifetime Capital Gains Exemption (LCGE):

- Reverse earnouts accelerate capital gains into the year of sale

- Allocation across multiple shareholders, trusts, or family members must be planned carefully

- Earnouts may provide timing flexibility, but introduce uncertainty

These considerations should be addressed early, not after price mechanics are agreed.

Asset Sales: A Cautionary Note

Earnout planning is significantly more difficult in asset transactions:

- Cost recovery is generally unavailable

- Contingent proceeds are more likely to be treated as income

- Vendors lose much of the tax deferral flexibility available in share sales

As a result, earnouts are often less attractive to vendors in asset deals.

Final Thoughts

Earnouts and reverse earnouts are powerful—but very different—tools. In Canada, small structural differences can drive materially different tax outcomes.

- Vendors prioritizing certainty and capital gains treatment may favour a properly structured reverse earnout

- Buyers seeking downside protection may prefer a traditional earnout

- In all cases, success depends on early tax planning, disciplined drafting, and alignment between economics and legal form

Disclaimer

This article is provided for general informational purposes only and does not constitute legal or tax advice. The tax treatment of earnouts and reverse earnouts depends on the specific facts and circumstances of each transaction. Parties should obtain independent tax and legal advice before implementing any transaction structure.

.jpg)